The Commission has finally released a study on the impact of its F2F and Biodiversity Strategy proposals on the agriculture sector.

The key commitments that directly affect the EU farming sector include reducing the use of chemical pesticides by 50% and of fertilisers by 20%, setting of at least 10% of agricultural area under high-diversity landscape features and of at least 25% under organic farming.

The results are staggering: supply is reduced by 10-15% in the key sectors, cereals, oilseeds, beef, dairy cows; over 15% in pork and poultry, and over 5% in vegetables and permanent crops.

The EU net trade position worsens (with the notable exception of dairy, as less use for animal feed and improved genetics would more than compensate for the sharp drop in the dairy herd).

Revenues plummet, with the exception of vegetable and permanent crops, and pork (due to sharp price increases that we discuss further down), with an average of 2 500 to 5 000 € drop per holding (subsidies included). The most penalized would be cereal growers and dairy farmers (-5 000 €), with lesser revenue cuts for the other sectors. Fruits and vegetables revenues would increase around 2 500 €, and pork up to 10 000 €.

The positive impact in reducing GHG emissions by less than 30% is leaked at least by half, as the EU increases imports and therefore the rest of the world increases production.

To put it concisely, lots of pain for little gain.

The study results are similar to a USDA-ERS impact assessment that found that the Commission proposals would reduce EU agriculture production by 12%, increase prices by 17%, reduce exports by 20%, increase imports by 2%, shrink gross farm income by 16%, and increase the annual per capita food cost in the EU by 130 euros.

Farm Europe also recently published an evaluation of the Commission proposals showing that production would experience a significant and rapid decline, -12% for wheat, -10% for maize, -7% for beet, -25% for oilseeds, -7% for red meat, -4% for milk, -1% for pork, -3% for poultry. That will generate a reduction in exports by 20%, and a significant increase in imports of plant proteins (soya) to cope with the decline in European oilseed production, contrary to the European incantations of a protein plan for greater autonomy of the European Union and the fight against imported deforestation. Agricultural incomes would fall by more than 8% in such a scenario.

All the analysis published show similar results, leaving little doubt that we would face a sharp policy driven contraction of agriculture in the EU.

Although in the study the Commission is at pains to lessen the staggering global negative impacts of its proposals, a closer look shows that most likely the impact would be harsher.

– Let’s begin by what is left out of the analysis: the Commission proposal to plant in good ecological conditions 3 billion trees. That would divert a lot of agriculture land to forestry. It could amount to between 1,5 to 2,7 million ha, depending on species and ecological conditions.

-Then come the rosy assumptions in the study. The expected increase in revenues for pork producers is contingent upon an expected uplift of pork prices by over 40%. Exports would somewhat decrease and imports raise, but far from the extent that would check such a dramatic price increase.

The way the model used in the study operates cannot capture real world trade dynamics, where imports out of quotas take place when the difference between EU and world prices is so high, and the quota rents are so hefty, that they become profitable despite the high out of quota tariffs.

Also beef prices are expected to jump over 20%, which in the real world would suck-in significant additional imports.

This problem is acknowledged in the study, without however leading to adjusting the results: “This was seen with the magnitude of price reactions when production falls significantly (i.e. meat activities), leading to the use of an additional model and change to some modelling assumptions for comparability. Even when undertaking sensitivity analysis, the price responses are large and the reaction of world markets is potentially too rigid to capture their adaptation capacity, especially in the long run”.

– In addition the study does not capture the likely impact of Brexit, in reducing our exports to an UK market open to third countries. Our exports of meats, dairy and other products will most likely fall, and that will depress both the EU production, prices and farmers revenues. Let’s not forget that the UK is a lead export market for the EU, our losses in that market will have a huge impact.

– Another area where the study assumptions are too optimistic is on the adoption of mitigation technologies, like precision farming and anaerobic digesters, key to reducing GHG emissions. The study assumes that the New Generation EU budget for the sector, which in the study assumptions would reduce mitigation technologies investment costs by 30%, is actually the double of what was decided – 15 billion vs 8.1 billion euros. Assuming that 60% of the EU agriculture would be using precision farming in 2030 seems overly optimistic, all the more as farmers revenues are expected to drop. How to expect investments to go up so much and so quickly when farmers would be worse off than today?

This has in turn a significant impact on the actual GHG reductions expected. Mitigation accounts for half of all GHG reductions, and precision farming and other mitigation technologies are the second most important contributor.

A more sober and less embarrassed analysis by the Commission, would show even steeper production and revenue cuts. As the net trade impact would be event worst, and the adoption of mitigation technologies more modest, the reduction of GHG emissions would be lower and show an even higher leakage as the EU would have to import more.

And thus, even more pain for lesser gains.

To conclude, the Commission Farm to Fork and Biodiversity Strategy proposals would cause an unprecedented fall in the EU’s agriculture production, a sharp cut in farmers’ revenues, a degradation of the bloc’s net trade position, and an increase in producer prices that would raise food costs for consumers. The environmental benefits would be mostly leaked, as EU imports would increase triggering higher GHG emissions in the rest of the world.

Ultimately, the way the European Commission is currently planning to implement the Green Deal objectives in agriculture would result in a global impoverishment of the sector and of European rural areas, a weakening of our food security, and an inflation of consumer prices. Agricultural sectors would face massive restructuring, with the abandonment of the least productive lands and a drastic reduction in the number of farms. It is hard to fathom a worst case scenario.

The Summer months have been full of international attention to food policies: starting in July, with the to the UN Food System Pre-Summit held in Rome, where civil society, private sector businesses, decision-makers and other stakeholders met to discuss the issues of transforming the global food systems, in preparation to the Food System Summit to be held in September in New York. The FAO proposed a voluntary code of conduct for businesses for food losses and food waste, and published its report on the state of nutrition of the world, underlying the devastating effects of the Covid-19 pandemic on hunger and malnutrition. At the European level, the EFSA opened a public consultation on minimum sugar levels in diet, and the European Parliament’s Special Committee on Beating Cancer adopted the first draft report of the EU Strategy on Beating Cancer.

While August has been a quiet month, July has seen some movements as regarding the Farm to Fork Strategy sponsored by the services of the European Commission. An unofficial impact assessment of the strategy has been published during the holidays considering the impacts of the targets on the EU agri-food markets, together with a report analysing the implementation of the “One Health” action plan on animal welfare and antimicrobial resistance; MEPs from ENVI and AGRI Committees agreed on amendments to the strategy texts, while in the Council of the EU consensus was found on the Organic Action Plan, during the first meeting under the Slovenian Presidency.

In the summer months, genomic techniques have been the centre of some quite debates: amongst others, the US Department of Agriculture proposed to exempt some gene edited plant varieties from the biotechnology law; a study has analysed how these technologies are perceived by the public, concluding that the purpose for which are used plays an important role for their acceptance; and the European Parliament has once again voted against the imports of GE plants. WHO published recommendation on human genome editing.

The Green Energy Platform (GEP) welcomes the level of ambition and the fact that renewable energy from EU agriculture (i.e. biofuels & biomethane) is recognised as an essential lever for achieving the objectives of the draft « Fit for 55 » package, in particular for transport, which is the most challenging sector to decarbonise.

However, it should be underlined that without an adequately increased contribution from sustainable bioenergy the proposed targets are simply impossible to meet. The proposed changes by the European Commission represent a major restructuring not only for the stakeholders concerned, but also for all EU citizens, as the changes will have a significant impact on everybody’s life and how they manage economically, no matter their status or whereabouts. Therefore, the cost of the transition should be a primary concern for EU decision-makers – as should the capacity of EU agriculture to strengthen EU’s independency in both food and energy. Potential redistribution via social funds are most welcome, but should not prevent EU institutions from making cost-effective energy choices for a fair transition that works for all.

The co-legislators should now build on the initial proposals tabled by the European Commission, strengthening further the contribution of renewables from EU agriculture, which are sustainable, affordable and free from deforestation effects. Renewables from EU agriculture are good for farmers, for society as a whole and for Europe’s sovereignty.

In order to bring the transition from concept stage to concrete viability this decade, with tangible GHG emission reductions on the ground, the Green Energy Platform recommends that :

– The market distorting multipliers, which have now been mostly cleansed from the text, should stay out of the proposals, while standards for assuring fraud prevention should be greatly strengthened further.

– Solutions that are already available, turning ambitions into climate action success by abating carbon today, must be further promoted by lifting unnecessary discriminations between Member States regarding their shares of biofuels consumed in transport.

– A Well-To-Wheel approach should be adopted instead of the outdated Tank-to-Wheel methodology, to be able to effectively take into account the impact of the full chain on GHG emissions.

– As the ultimate objective is the reduction of GHG emissions with the promotion and facilitation of the uptake of renewable energy, the revision of fuel standards is also critical. The current limit on the blend wall for bioethanol and biodiesel should be modified upwards, given that it represents one of the most simple and cost effective options for further reducing GHG emissions.

Furthermore, it should be remembered that European sourced biofuels and biomethane bring multiple added benefits beyond decarbonisation, such as boosting Europe’s food security by co-producing valuable by-products, and supporting farming communities via income stabilisation opportunities which are essential for the agricultural transition.

Now is the time to move forward with a finally solid framework for bioenergy, that unleashes its true potential, provides sustainability peace-of-mind, enables necessary changes, and not only represent attractive policy objectives, but realistically takes into consideration the real costs and GHG savings profiles of Europe’s decarbonisation strategies.

In June the agriculture Committee in the European Parliament discussed the Commission’s study on New Genomic Techniques for which many MEPs showed their support. Also, in Germany, the main political parties exposed their political manifestos and took public position on the matter of NGTs. Scientists from Freibourg University pioneered a method that allows for the insertion of specific genetic information into specific genes. All along, the European Investment Bank signed a loan for investments in non-GMO seeds.

After the ‘Nestlégate’, which saw the Swiss food multinational admitting that a big majority of its products cannot be considered “healthy”, the UK is taking further steps in limiting the advertisement of unhealthy foods to children, and a pilot project for eco-label is planned to take off in the autumn, in France. Yuka, the food-shop adviser app, has been found guilty of ‘acts of denigrations’ in a legal battle against the French Charcuterie Producers association. At the European level, the future Research & Innovation Common Programme for the financial period, Horizon Europe, will assign €32 million for sustainable protein research.

During the last decades, the European wine sector has been able to keep up with the increasing competition both in the domestic and in the world’s markets. It built its strategy on enhanced quality & productivity, while meeting higher environmental and sustainability standards which were becoming an always more important aspect of the product.

In a context where the EU exports in the global market have being losing around 10 percentage points a year, in which the domestic consumption has been falling by 30% in the last few years while the imports of non-EU wine were on the increase, wine cooperatives have been able to strive and rebound.

This has been possible due to a combination of, on the one hand, the resilience of the European producers, who were able to adapt and innovate, to build on the solid foundation of EU traditions, and, on the other hand, to the vision and strength of the public support policies intended to promote the European way of producing and enjoying wine worldwide while protecting the local savoir-faire.

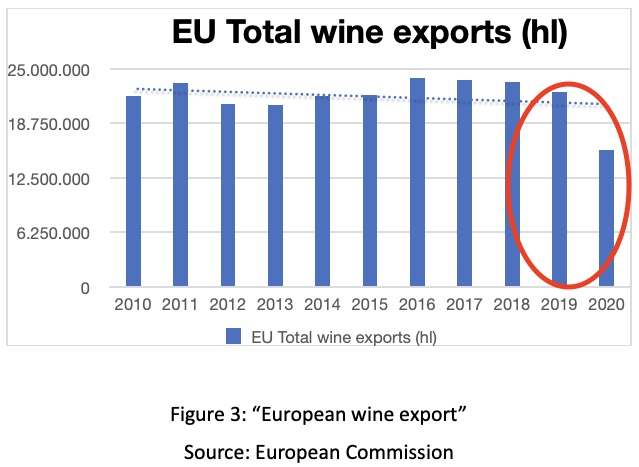

However, the EU wine sector is now at the tipping point and cannot afford to rely on its past achievements anymore. The Covid-19 restrictions and the consequent closing of the HoReCa sector meant a drop in export of 30%, while due to the cumulative impact of Covid and of the implementation of the China-Australia Free trade agreement, the EU exports to China have been reduced by almost 57%, not to mention the impact of Brexit.

In addition to these economic challenges, the wine sector is one of the first affected by climate change, as recent frost waves reminded. The multiplication of extreme weather conditions has a direct impact on wine production.

Therefore, without a new impetus, the EU wine sector risks to lose its position as a global leader that creates trends, markets, and prices. The wine is still perceived as the case study for success stories in the EU agricultural sector, but this perception must not overshadow the challenges to overcome. To keep its position as a locomotive for Europe, urgent actions are needed to support it, questioning the status-quo and building new strategies.

Many decision leaders, notably from the European institutions admitted the dire situation the EU wine sector lies right now:

Commissioner Wojciechowski, “the wine sector has been among the sectors hit the hardest by the coronavirus crisis and the related lockdown measures taken across EU”. The loss “was not compensated by home consumption”.

Former Italian Agriculture Minister Teresa Bellanova reminded that “to the structural market difficulties, the Covid-19 pandemic was added, which left deep wounds”.

At the same time, social and economic sustainability will be needed in order to achieve the environmental one, as MEP Anne Sander (FR, EPP) put it: “the economic aspects and sustainability are the two faces of the same coin […] we need both to guarantee the environmental and climate one”.

MEP Pina Picierno (IT, S&D) said that the “picture is particularly bad. The wine sector is suffering […] because of the pandemic, the HoReCa closing, the tariffs”.

Europe needs a plan

”We implemented several aids […] since this summer to help the industry. However, we already know that, at a certain point, they will not be enough”, Julien Denormadie, French Agricultural Minister, echoing many Member States (cf Council’s documents for similar declaration of the delegation of Bulgaria, Croatia, Slovakia among others).

MEP Tolleret (FR, Renew): “the good state of the market before the Covid crisis […] showed that the political choices were appropriate [for the sector]”.

President of the Spanish Cooperatives, Angel Villafranca: “we cannot face an extraordinary situation with ordinary tools”.

Francisco Martinez Arroyo, adviser for the Spanish Castilla-la Mancha government: “the sector needs [additional support] more than ever in this moment”, “If we only got additional funds, that should not be taken from other tools”.

Global trends and competition (“New world”), tariffs, Brexit, Covid-19 pandemic, and climate change are posing serious threats to European wine producers, and, therefore, to the economic and cultural influence of the sector.

Today, an EU economic recovery and climate adaptation plan for the next three years is needed with no delay.

It will take at least 2 years to relaunch the dynamics of the demand. The crisis has profoundly disrupted consumer habits, making the path of complete recovery longer and more difficult. It is, therefore, high time to act both on internal consumption and focus on exports. At the same time, recovering from the economic crisis must support the ecological transition to respond to climate change.

Adequate means are needed to respond properly to the crisis and the challenges of the near future.

First of all, the extension of the crisis measures for the whole of 2021 & 2022 is needed. In fact, the crisis measures will be in place until October 2021, but this delay will not be enough to cover the expenses related to production, stockage and distribution of the ongoing production. Subsequently, the national support programs must be enlarged and financed with a substantial budget. It is not credible to imagine that emergency measures can be financed within the existing PNA budgets. That would mean delaying the structural actions that the EU wine sectors needs to prepare for its future.

Current crisis measures are still needed but not enough.

A multi-annual plan is also required to give priority to viticulture and to bring additional economic resources:

Exceptional storage and distillation measures for 12 months to smooth out the marketing of the large stocks that have built up due to the closure of the HoReCa and export markets over the past two years.

Massive investment plan on innovation to assure the transition of the wine production chain towards precision viticulture. Investments at vineyard level to increase competitiveness, in particular to stop losing market share on medium range markets. The priority should be given to old and unirrigated vineyards so to increase the quality of the production and its competitiveness.

Increased actions aiming at re-gaining markets’ shares and to open new ones: strengthen the funds dedicated to the promotion of European wines in exports and increase communication on the domestic market, notably by underlying the tools and efforts that EU wine producers are making in order to increase the sustainability of their production. Consolidate existing markets and reconquer market shares on medium range markets which are the priority of New World producers.

Investment plan in research of new breeds, notably on New Genomic Techniques as a tool to face the challenges related to climate change and consumption expectancies.

Investment plan to tackle the water access challenge and face water scarcity in most wine producing regions.

Key economic indicators

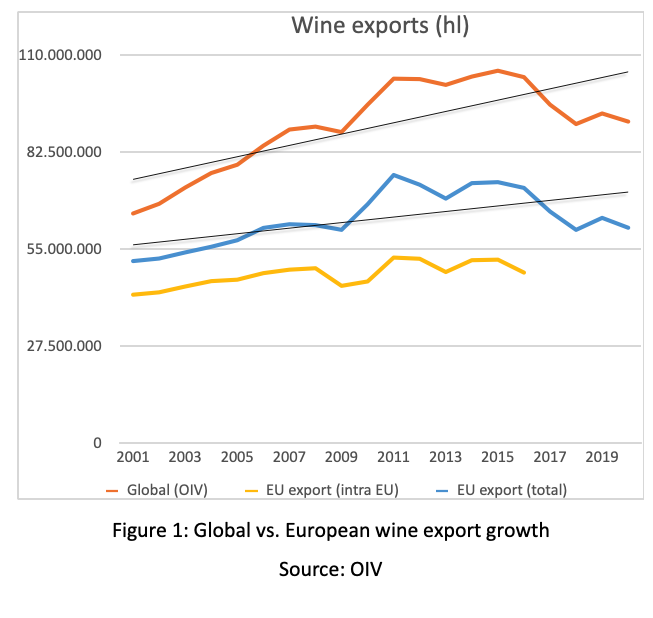

The general trend shows a growing market for EU wines exports since the beginning of the 2000’s. However, this has been possible only because the global trend has been improving as well, making the EU growth, relatively little (Figure 1).

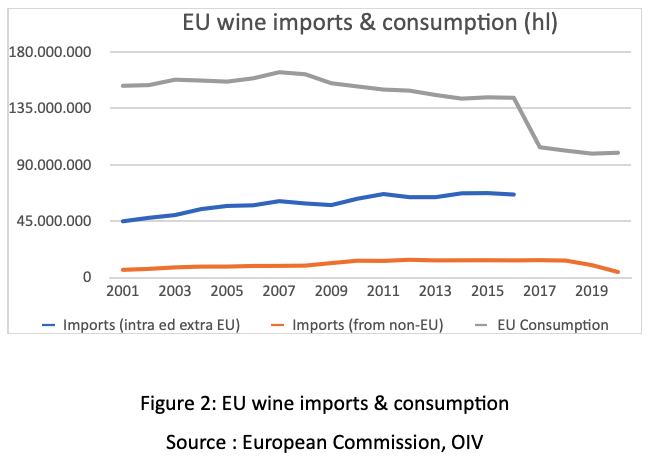

Since the beginning of the 2000’s the European growing exports rates have been relatively decreasing if compared to the world’s one. The EU has been losing its presence on the global market, being replaced by other competitors. In 2001 the EU total wine trade represented 79% of the global one. In 2016, it represented 70% despite the constant growth in its exports. In other words, if at the beginning of the century the non-European section of wines that were present in the global market was between 13 mhl and 20 mhl, nowadays the figure increased to more than 30 mhl. In parallel, on the domestic market, while imports from non-EU countries have been increasing, European consumption has been constantly falling. In particular, starting from 2008/09, to a soft peak of imports it follows a slow but constant decreasing level of EU wine consumption (Figure 2). Non-EU wines are increasingly present on Europeans’ tables, at the expenses of European production.

Both the external (exports) and the domestic (imports) data show that European wines are losing markets’ shares in favour of third-countries products. This situation requires a strong response, notably with the draft of an action plan designed to give dynamism to the EU wine industry.

Key COVID indicators

As if these external threats were not enough, in 2020 the whole world has been hit hard by the Covid pandemic which, besides the human catastrophe, it came with an economic one. Despite the resilience that EU farmers showed during the crisis, without letting people down on their expectations to supply food, many agricultural businesses, notably SMEs, faced the worst of the consequences. In particular, the activities strongly related to the HoReCa industry, have been forced to stop their usual distribution channels. Due to that, estimates talk about a loss of 30% of the volume and 50% of the value sold in the EU. Exceeding stocks, reduction of selling capacity, reduced purchase power of consumers, reduced exports and consumption, decreased tourism, cancellation of events and festivals are some of the consequences that Covid-19 restrictions had on the wine sector. The restrictions imposed by governments led to an abrupt change in the purchasing behaviour of consumers and, therefore, a sudden change required by producers as well: sells from wine specialty stores dropped by 35%, exports by 36%, and 91% from restaurants and hotels. While 77% of the hotels & restaurants had to close (at least temporarily), 25% of wine businesses followed the same destiny, with almost 60% of wine businesses reporting economic losses due to Covid-19 (70% of the businesses were small wineries). Despite the increase in the online selling channels, most of the wineries could not compensate the losses from the important reduction of HoReCa, exports, and tourism. This is a “demand crisis”, said MEP Paolo DeCastro (IT, S&D) “andwe will have to face it as such”.

Climate Change impact on vines

Wine is at the forefront of the climate challenge, with urgent need of adaptation. There is a direct link between the specificity of the products and climate conditions. Climate variations have major impact on quality, and urgently call for innovation, new varieties, etc.

Climate change is another difficult threat to overcome. On one hand the natural events that are the consequence of global warming are more and more unpredictable, what it makes it more difficult for a wine grower to prepare (tools, assurance, etc.), to recover, and to plan (leading to uncertainties when it comes to business planning and consumer relations). On the other hand, transition towards production methods that would reduce, or even nullify, the negative impacts on the environment & biodiversity, while improving wine production and quality require high investments and redesign efforts. Climate change affects agricultural production as a whole and while action has to be taken to target the core of the issue (middle-to-long-term target), producers should also be able to face current events that put them on the brink of going out of business.

In recent months, the unusual frost wave that touched the majority of Western and part of the Central and Southern Europe during the month of April 2021 had devastating effects on agricultural production, notably on the vines, leaving vine growers, already concerned by the Covid pandemic economic crisis, in an even greater state of incertitude. Many of us were not covered by insurance against frost. Climatic events have been hitting the sector since 2017, where yields had suffered from another frost wave, in 2018 when they were hit by mildew, and from the heatwave in 2019.

We joint the call of the co-chair of the EU Parliament intergroup on wines, MEP Tolleret (FR, Renew), when she says that “at the European level, climatic insurances are not sufficient”, calling for European reinforced support to insurance scheme for wine growers.

Global scenario

With a look at the international markets, it is important not to forget the consequences of more than a year of trade war (introduced in October 2019) against the EU biggest importer of wine, due to the Boeing-Airbus issue. In this context, the US authorities imposed a 25% ad valorem punitive tariff on EU wines, that resulted in a 54% drop in exports of the targeted wines. The estimated loss for the EU wine exports derived from the trade war amounts to a drop in the 2019/20 campaign of 10% (or €8 billion), what led French Agriculture minister to say that “this is a disaster for our vine growers”. In this context, the cooperative model has shown its resilience and capacity to overcome the challenges with creativity and endurance. Confronted with the “Trump taxes” we managed to develop alternative markets, for example via BagInBox solutions to maintain volumes exported. Even if the recent developments in the Transatlantic trade relations have unfolded positive news for the economic sectors that have been involved in the trade war (a five-years truce has been agreed upon), if we consider the scale of the cumulative effects of climate, trade and economic tensions, the wine sector urgently needs support from EU decision-makers.

Still on global trade issues, it is worth also to mention the relations between China and Australia as an example of the unpredictable exogenous forces that drive global trade relations and that cannot, by definition, be controlled. In fact, after the implementation of a Free Trade Agreement (starting in 2015) for which direct tariffs on wine have been reduced, the EU wine sector has seen its share of the Chinese market drop, with negative economic consequences on the European businesses. However, recent disputes between the two Asian partners on trade issues have been involving the wine sector as well, damaging, notably, the Australian exports of wine to China (that, after the FTA have come to represent more than a third of China’s wine imports, for a value of almost €1,9 billion annually). Following a 200% Chinese tariff of Australian wines, these have dropped by 96% between December 2020 and March 2021 compared to the previous year, halting, as a matter of fact, Australia’s wine trade to its biggest commercial partner. This situation is forcing the 37% of Australian exports that normally goes to the Chinese market to find alternative markets to release the pressure. If this surely represents a threat to our European industry, it also represents an opportunity for us to insert our products in the Chinese market as a supplement for the missing Australian beverage. This example underlines the unpredictable dynamics of global trade relations on which we so strongly depend on, given the high export-oriented sector we work in, and considering that in the close future exports will represent a higher share of our trade if we take into account the decreasing consumption rates within the EU. In order to succeed in the export markets, beside a strong promotion policy, we need to know what the future holds for us, meaning that stability in the EU trade policy is of outmost importance for assuring a healthy European wine industry. In this context, we call for a stronger commitment of the EU to develop even further trade relations with historic and new partners setting the base for improved conditions for the sector in current and future Free Trade Agreements. To this respect, we welcome and support the initiative of the Commission to review the EU Trade Strategy hoping that it will renew and defend the dynamism of our wines.

On a more continental scale, Brexit represents a close-by threat that seems to have been forgotten. The UK market for wine, in fact, represented 22% of the EU exports in 2019, and its imports from Europe (between 55% and 60%, worth around €1.8 billion) are at risk. With the trading issues deriving from the separation of the UK from the EU, the increasingly time-consuming paperwork, tariffs, and costs, we found ourselves in a funnel whose unblock seems very unlikely. Despite the efforts done in the years of negotiation of the Brexit deal, the trade impact that the current accord has on the European wine industry is detrimental. Even if Brexit has come into effect “only” in January 2021, its impact can already be perceived from us on the field. This can no longer be the case.

The EU Green Deal and Europe’s Beating Cancer Plan

The European Green Deal can be an opportunity or a threat for the European wine sector depending on how it is implemented. About 50 proposals will be put forward in the coming months having direct and indirect impact. While the environmental objectives are widely supported, the policy path will be a major challenge: it can lead to constant de-growth with extra constraints and administrative burdens, or on the contrary, to a double performance strategy that responds to societal expectations and promotes economic and environmental growth. If, as we hope, the outcomes will be closer to the latter scenario, we will be asked to invest in new technologies, patterns, and tools to comply with the demanding and needed changes that are foresaw. To that end, increased public support will be needed to our sector in order to accompany the wine value chain in this transition.

The input reduction strategy and the labelling initiatives will be the most important initiatives for the sector. For both, science and innovation must be mobilised. This should also apply for the Commission’s Beating Cancer Plan. As such, moderation in the consumption of every product is what makes a diet balanced, not the demonization and, therefore, the exclusion of some of them.

Irène Tolleret, MEP: “In order to fight against cancer, I think that we can implement positive actions instead of applying an approach based on the demonization of certain products. […] the main problem is in abusive consumption. All in all, any ban will lead to the transgression of the rules”.

Several scientific studies confirm the positive effects on health of moderate wine consumption in the context of balanced diet and regular physical activity. Its effects have been analysed on cardiovascular diseases, metabolism, thrombosis, hypertension, renal & neurodegenerative diseases, diabetes and cancer and it seems that “all these data, rather controversial, lead us to think that the beneficial effects could be due to both to polyphenols and alcohol”

As many scientific studies show, in fact, moderate consumption of wine, which is an important element of the Mediterranean diet as such, has positive consequences on the general health of the one who consumes it – surely within the context of a balanced diets and regular physical activity-. Communication campaigns aimed at educating the public to the benefits of moderate consumption of every product should be considered, given the fact that promoting the absolute abstention of any product never resulted in the expected outcome.

Recommendations

In this complex context, us, European wine farmers, have been acting in our best efforts, trying to come up with creative ideas by strengthening our adaptability. However, we have been feeling the absence of our long-standing partner in the success story that European wine has become. The European Commission in these past months has remained silent and deaf to our calls. Whatever the threat, being the Covid pandemic, climatic disasters, trade war, Brexit, the only answer that we have been receiving from its services is “there is simply no money”, answer that has been reiterated recently after the frost wave.

This answer is simply not credible nor understandable, considering the amounts of funds that the EU has moved for other strategic sectors and the importance of the economy generated by our industry for more than 50 regions and the EU in general, representing 2.5 million works, more than half of the European trade balance, and the image of the EU agri-for products, whose wines are the best ambassadors.

A renewed private-public partnership as secret of success

The duo private-public has shown its potential when cooperating over the last two decades, putting back on promising track the wine economy, overcoming the challenge of the new world production. It is now the time to write a new success story, building the foundation of a new cooperation for the benefit of jobs, economy, environmental features and protection, and European identity.

It is therefore urgent for the European Commission to take actions, complementary to those initiative taken at local, regional, or at national level.

Call for Proposals: A Website Brief for web developers

PAPILLONS is a Horizon project of 20 partners within a consortium selected and funded by the European Commission to be implemented. The creation and maintenance of a Website is foreseen within the Project with the aim for information display and exchange featuring communication, dissemination and exploitation activities for public outreach and stakeholder engagement.

The aim of this briefing file is to inform potential professional web developers to design the website with what is required for the PAPILLONS website for further discussions to be able to foresee how this could be implemented.

More information on the call for Website developers are available in the following file:

Farm Europe welcomes the agreement on the reform of the Common Agricultural Policy reached today. It preserves the common dimension of this policy and it provides the means to give impetus to a real economic and environmental ambition, clearly improving the European Commission’s initial proposal. The tireless work of the Portuguese Presidency, of long-established MEPs such as Peter Jahr, Anne Sander, Paolo de Castro, Nobert Lins and Herbert Dorfmann, and of newcomers in the European Parliament CAP negotiations such as Martin Hlavácek,Pascal Canfin, Pina Picierno, Jeremie Decerle and Irène Tolleret, each of whom played a key role in structuring constructive and ambitious positions within the European Parliament and then in the inter-institutional negotiations must be commended. The final compromise provides a clear framework for Member States to implement a strategy for the economic and environmental transition of the agricultural sector in order to provide quality food for all Europeans and to allow farmers to invest and innovate, using the following tools:

With the “eco-schemes“, the European Union now has an its disposal an incentive tool to help European farms to adapt to climate change, store carbon, enrich biodiversity, be less dependent on inputs and enhance animal welfare. This tool will prove its effectiveness when used to achieve the twin goals of more economically and environmentally efficient farming. The point-system should ensure a level playing field across Europe and within Member States in the ambition and implementation of the different eco-schemes.

With “green investments” earmarked as a priority in the second pillar of the CAP, and the ability of all sectors to implement operational programs funded by the first pillar of the CAP, this reform sends the signal that it is through innovation and investment that the European Union will succeed in achieving the ambition set in the Farm to fork Strategy and the Green Deal. These investments must make it possible to achieve the environmental objectives while gaining in economic competitiveness and preventing competition from third countries to develop.

With the crisis reserve of at least €450 million and the possible earmarking of 3% of the first pillar of the CAP for risk and crisis management tools, the economic nature and reactivity of the CAP in response to unforeseen events are potentially reinforced. It will be important for the Member States to seize these levers and for the Commission to activate the tools at its disposal in the event of a crisis without delay and without procrastination.

On this basis, the European agricultural sector has a certain visibility, which is imperative for the years to come, with a strong responsibility now resting on:

the shoulders of the Commission to validate the national strategic programs by ensuring their consistency with the guidelines defined at European level and by limiting the distortions that could arise from divergent approaches between Member States.

the shoulders of the Member States to fully activate the tools designed by the European Parliament and the Council in order to strengthen the European agricultural sectors and prepare their future by putting a clear priority on innovation investments and risk management.

the shoulders of the co-legislators to make sure that the regulations of the F2F reinforce the orientations decided by the co-legislators in the CAP and do not contradict them.

It is regrettable, however, that food chain issues, notably those related not only to digitalization and blockchain, but also to the food and nutritional dimension in particular, have not found their place in this reform. It is to be hoped that these topics will be addressed in an effective and coherent way with the CAP in the framework of future proposals from Farm to Fork, in order to meet the expectations of all consumers, by rejecting the model of a multi-speed food supply according to purchasing power.