After the ‘Nestlégate’, which saw the Swiss food multinational admitting that a big majority of its products cannot be considered “healthy”, the UK is taking further steps in limiting the advertisement of unhealthy foods to children, and a pilot project for eco-label is planned to take off in the autumn, in France. Yuka, the food-shop adviser app, has been found guilty of ‘acts of denigrations’ in a legal battle against the French Charcuterie Producers association. At the European level, the future Research & Innovation Common Programme for the financial period, Horizon Europe, will assign €32 million for sustainable protein research.

During the last decades, the European wine sector has been able to keep up with the increasing competition both in the domestic and in the world’s markets. It built its strategy on enhanced quality & productivity, while meeting higher environmental and sustainability standards which were becoming an always more important aspect of the product.

In a context where the EU exports in the global market have being losing around 10 percentage points a year, in which the domestic consumption has been falling by 30% in the last few years while the imports of non-EU wine were on the increase, wine cooperatives have been able to strive and rebound.

This has been possible due to a combination of, on the one hand, the resilience of the European producers, who were able to adapt and innovate, to build on the solid foundation of EU traditions, and, on the other hand, to the vision and strength of the public support policies intended to promote the European way of producing and enjoying wine worldwide while protecting the local savoir-faire.

However, the EU wine sector is now at the tipping point and cannot afford to rely on its past achievements anymore. The Covid-19 restrictions and the consequent closing of the HoReCa sector meant a drop in export of 30%, while due to the cumulative impact of Covid and of the implementation of the China-Australia Free trade agreement, the EU exports to China have been reduced by almost 57%, not to mention the impact of Brexit.

In addition to these economic challenges, the wine sector is one of the first affected by climate change, as recent frost waves reminded. The multiplication of extreme weather conditions has a direct impact on wine production.

Therefore, without a new impetus, the EU wine sector risks to lose its position as a global leader that creates trends, markets, and prices. The wine is still perceived as the case study for success stories in the EU agricultural sector, but this perception must not overshadow the challenges to overcome. To keep its position as a locomotive for Europe, urgent actions are needed to support it, questioning the status-quoand building new strategies.

Many decision leaders, notably from the European institutions admitted the dire situation the EU wine sector lies right now:

Commissioner Wojciechowski, “the wine sector has been among the sectors hit the hardest by the coronavirus crisis and the related lockdown measures taken across EU”. The loss “was not compensated by home consumption”.

Former Italian Agriculture Minister Teresa Bellanova reminded that “to the structural market difficulties, the Covid-19 pandemic was added, which left deep wounds”.

At the same time, social and economic sustainability will be needed in order to achieve the environmental one, as MEP Anne Sander (FR, EPP) put it: “the economic aspects and sustainability are the two faces of the same coin […] we need both to guarantee the environmental and climate one”.

MEP Pina Picierno (IT, S&D) said that the “picture is particularly bad. The wine sector is suffering […] because of the pandemic, the HoReCa closing, the tariffs”.

Europe needs a plan

”We implemented several aids […] since this summer to help the industry. However, we already know that, at a certain point, they will not be enough”, Julien Denormadie, French Agricultural Minister, echoing many Member States (cf Council’s documents for similar declaration of the delegation of Bulgaria, Croatia, Slovakia among others).

MEP Tolleret (FR, Renew): “the good state of the market before the Covid crisis […] showed that the political choices were appropriate [for the sector]”.

President of the Spanish Cooperatives, Angel Villafranca: “we cannot face an extraordinary situation with ordinary tools”.

Francisco Martinez Arroyo, adviser for the Spanish Castilla-la Mancha government: “the sector needs [additional support] more than ever in this moment”, “If we only got additional funds, that should not be taken from other tools”.

Global trends and competition (“New world”), tariffs, Brexit, Covid-19 pandemic, and climate change are posing serious threats to European wine producers, and, therefore, to the economic and cultural influence of the sector.

Today, an EU economic recovery and climate adaptation plan for the next three years is needed with no delay.

It will take at least 2 years to relaunch the dynamics of the demand. The crisis has profoundly disrupted consumer habits, making the path of complete recovery longer and more difficult. It is, therefore, high time to act both on internal consumption and focus on exports. At the same time, recovering from the economic crisis must support the ecological transition to respond to climate change.

Adequate means are needed to respond properly to the crisis and the challenges of the near future.

First of all, the extension of the crisis measures for the whole of 2021 & 2022 is needed. In fact, the crisis measures will be in place until October 2021, but this delay will not be enough to cover the expenses related to production, stockage and distribution of the ongoing production. Subsequently, the national support programs must be enlarged and financed with a substantial budget. It is not credible to imagine that emergency measures can be financed within the existing PNA budgets. That would mean delaying the structural actions that the EU wine sectors needs to prepare for its future.

Current crisis measures are still needed but not enough.

A multi-annual plan is also required to give priority to viticulture and to bring additional economic resources:

Exceptional storage and distillation measures for 12 months to smooth out the marketing of the large stocks that have built up due to the closure of the HoReCa and export markets over the past two years.

Massive investment plan on innovation to assure the transition of the wine production chain towards precision viticulture. Investments at vineyard level to increase competitiveness, in particular to stop losing market share on medium range markets. The priority should be given to old and unirrigated vineyards so to increase the quality of the production and its competitiveness.

Increased actions aiming at re-gaining markets’ shares and to open new ones: strengthen the funds dedicated to the promotion of European wines in exports and increase communication on the domestic market, notably by underlying the tools and efforts that EU wine producers are making in order to increase the sustainability of their production. Consolidate existing markets and reconquer market shares on medium range markets which are the priority of New World producers.

Investment plan in research of new breeds, notably on New Genomic Techniques as a tool to face the challenges related to climate change and consumption expectancies.

Investment plan to tackle the water access challenge and face water scarcity in most wine producing regions.

Key economic indicators

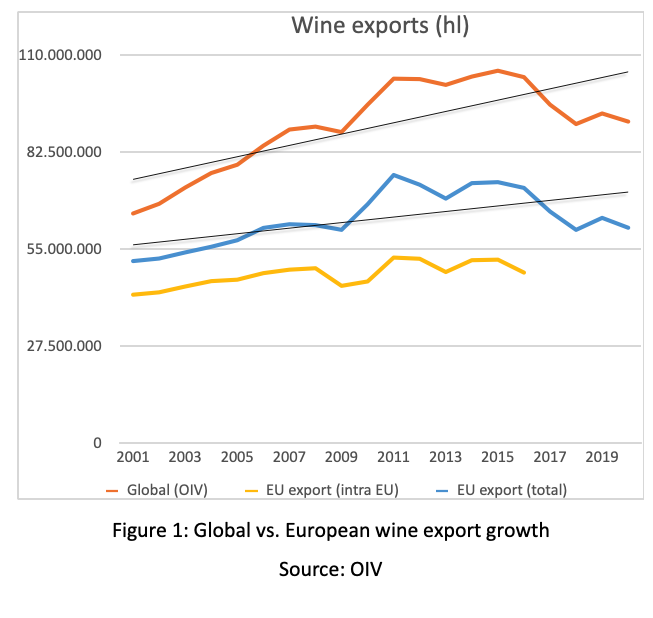

The general trend shows a growing market for EU wines exports since the beginning of the 2000’s. However, this has been possible only because the global trend has been improving as well, making the EU growth, relatively little (Figure 1).

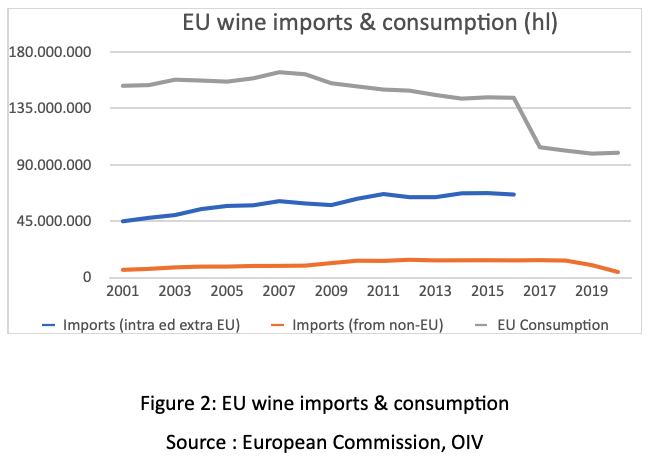

Since the beginning of the 2000’s the European growing exports rates have been relatively decreasing if compared to the world’s one. The EU has been losing its presence on the global market, being replaced by other competitors. In 2001 the EU total wine trade represented 79% of the global one. In 2016, it represented 70% despite the constant growth in its exports. In other words, if at the beginning of the century the non-European section of wines that were present in the global market was between 13 mhl and 20 mhl, nowadays the figure increased to more than 30 mhl. In parallel, on the domestic market, while imports from non-EU countries have been increasing, European consumption has been constantly falling. In particular, starting from 2008/09, to a soft peak of imports it follows a slow but constant decreasing level of EU wine consumption (Figure 2). Non-EU wines are increasingly present on Europeans’ tables, at the expenses of European production.

Both the external (exports) and the domestic (imports) data show that European wines are losing markets’ shares in favour of third-countries products. This situation requires a strong response, notably with the draft of an action plan designed to give dynamism to the EU wine industry.

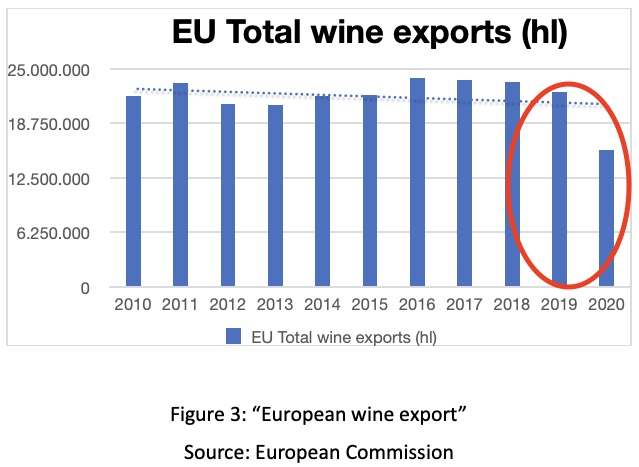

Key COVID indicators

As if these external threats were not enough, in 2020 the whole world has been hit hard by the Covid pandemic which, besides the human catastrophe, it came with an economic one. Despite the resilience that EU farmers showed during the crisis, without letting people down on their expectations to supply food, many agricultural businesses, notably SMEs, faced the worst of the consequences. In particular, the activities strongly related to the HoReCa industry, have been forced to stop their usual distribution channels. Due to that, estimates talk about a loss of 30% of the volume and 50% of the value sold in the EU. Exceeding stocks, reduction of selling capacity, reduced purchase power of consumers, reduced exports and consumption, decreased tourism, cancellation of events and festivals are some of the consequences that Covid-19 restrictions had on the wine sector. The restrictions imposed by governments led to an abrupt change in the purchasing behaviour of consumers and, therefore, a sudden change required by producers as well: sells from wine specialty stores dropped by 35%, exports by 36%, and 91% from restaurants and hotels. While 77% of the hotels & restaurants had to close (at least temporarily), 25% of wine businesses followed the same destiny, with almost 60% of wine businesses reporting economic losses due to Covid-19 (70% of the businesses were small wineries). Despite the increase in the online selling channels, most of the wineries could not compensate the losses from the important reduction of HoReCa, exports, and tourism. This is a “demand crisis”, said MEP Paolo DeCastro (IT, S&D) “andwe will have to face it as such”.

Climate Change impact on vines

Wine is at the forefront of the climate challenge, with urgent need of adaptation. There is a direct link between the specificity of the products and climate conditions. Climate variations have major impact on quality, and urgently call for innovation, new varieties, etc.

Climate change is another difficult threat to overcome. On one hand the natural events that are the consequence of global warming are more and more unpredictable, what it makes it more difficult for a wine grower to prepare (tools, assurance, etc.), to recover, and to plan (leading to uncertainties when it comes to business planning and consumer relations). On the other hand, transition towards production methods that would reduce, or even nullify, the negative impacts on the environment & biodiversity, while improving wine production and quality require high investments and redesign efforts. Climate change affects agricultural production as a whole and while action has to be taken to target the core of the issue (middle-to-long-term target), producers should also be able to face current events that put them on the brink of going out of business.

In recent months, the unusual frost wave that touched the majority of Western and part of the Central and Southern Europe during the month of April 2021 had devastating effects on agricultural production, notably on the vines, leaving vine growers, already concerned by the Covid pandemic economic crisis, in an even greater state of incertitude. Many of us were not covered by insurance against frost. Climatic events have been hitting the sector since 2017, where yields had suffered from another frost wave, in 2018 when they were hit by mildew, and from the heatwave in 2019.

We joint the call of the co-chair of the EU Parliament intergroup on wines, MEP Tolleret (FR, Renew), when she says that “at the European level, climatic insurances are not sufficient”, calling for European reinforced support to insurance scheme for wine growers.

Global scenario

With a look at the international markets, it is important not to forget the consequences of more than a year of trade war (introduced in October 2019) against the EU biggest importer of wine, due to the Boeing-Airbus issue. In this context, the US authorities imposed a 25% ad valorem punitive tariff on EU wines, that resulted in a 54% drop in exports of the targeted wines. The estimated loss for the EU wine exports derived from the trade war amounts to a drop in the 2019/20 campaign of 10% (or €8 billion), what led French Agriculture minister to say that “this is a disaster for our vine growers”. In this context, the cooperative model has shown its resilience and capacity to overcome the challenges with creativity and endurance. Confronted with the “Trump taxes” we managed to develop alternative markets, for example via BagInBox solutions to maintain volumes exported. Even if the recent developments in the Transatlantic trade relations have unfolded positive news for the economic sectors that have been involved in the trade war (a five-years truce has been agreed upon), if we consider the scale of the cumulative effects of climate, trade and economic tensions, the wine sector urgently needs support from EU decision-makers.

Still on global trade issues, it is worth also to mention the relations between China and Australia as an example of the unpredictable exogenous forces that drive global trade relations and that cannot, by definition, be controlled. In fact, after the implementation of a Free Trade Agreement (starting in 2015) for which direct tariffs on wine have been reduced, the EU wine sector has seen its share of the Chinese market drop, with negative economic consequences on the European businesses. However, recent disputes between the two Asian partners on trade issues have been involving the wine sector as well, damaging, notably, the Australian exports of wine to China (that, after the FTA have come to represent more than a third of China’s wine imports, for a value of almost €1,9 billion annually). Following a 200% Chinese tariff of Australian wines, these have dropped by 96% between December 2020 and March 2021 compared to the previous year, halting, as a matter of fact, Australia’s wine trade to its biggest commercial partner. This situation is forcing the 37% of Australian exports that normally goes to the Chinese market to find alternative markets to release the pressure. If this surely represents a threat to our European industry, it also represents an opportunity for us to insert our products in the Chinese market as a supplement for the missing Australian beverage. This example underlines the unpredictable dynamics of global trade relations on which we so strongly depend on, given the high export-oriented sector we work in, and considering that in the close future exports will represent a higher share of our trade if we take into account the decreasing consumption rates within the EU. In order to succeed in the export markets, beside a strong promotion policy, we need to know what the future holds for us, meaning that stability in the EU trade policy is of outmost importance for assuring a healthy European wine industry. In this context, we call for a stronger commitment of the EU to develop even further trade relations with historic and new partners setting the base for improved conditions for the sector in current and future Free Trade Agreements. To this respect, we welcome and support the initiative of the Commission to review the EU Trade Strategy hoping that it will renew and defend the dynamism of our wines.

On a more continental scale, Brexit represents a close-by threat that seems to have been forgotten. The UK market for wine, in fact, represented 22% of the EU exports in 2019, and its imports from Europe (between 55% and 60%, worth around €1.8 billion) are at risk. With the trading issues deriving from the separation of the UK from the EU, the increasingly time-consuming paperwork, tariffs, and costs, we found ourselves in a funnel whose unblock seems very unlikely. Despite the efforts done in the years of negotiation of the Brexit deal, the trade impact that the current accord has on the European wine industry is detrimental. Even if Brexit has come into effect “only” in January 2021, its impact can already be perceived from us on the field. This can no longer be the case.

The EU Green Deal and Europe’s Beating Cancer Plan

The European Green Deal can be an opportunity or a threat for the European wine sector depending on how it is implemented. About 50 proposals will be put forward in the coming months having direct and indirect impact. While the environmental objectives are widely supported, the policy path will be a major challenge: it can lead to constant de-growth with extra constraints and administrative burdens, or on the contrary, to a double performance strategy that responds to societal expectations and promotes economic and environmental growth. If, as we hope, the outcomes will be closer to the latter scenario, we will be asked to invest in new technologies, patterns, and tools to comply with the demanding and needed changes that are foresaw. To that end, increased public support will be needed to our sector in order to accompany the wine value chain in this transition.

The input reduction strategy and the labelling initiatives will be the most important initiatives for the sector. For both, science and innovation must be mobilised. This should also apply for the Commission’s Beating Cancer Plan. As such, moderation in the consumption of every product is what makes a diet balanced, not the demonization and, therefore, the exclusion of some of them.

Irène Tolleret, MEP: “In order to fight against cancer, I think that we can implement positive actions instead of applying an approach based on the demonization of certain products. […] the main problem is in abusive consumption. All in all, any ban will lead to the transgression of the rules”.

Several scientific studies confirm the positive effects on health of moderate wine consumption in the context of balanced diet and regular physical activity. Its effects have been analysed on cardiovascular diseases, metabolism, thrombosis, hypertension, renal & neurodegenerative diseases, diabetes and cancer and it seems that “all these data, rather controversial, lead us to think that the beneficial effects could be due to both to polyphenols and alcohol”

As many scientific studies show, in fact, moderate consumption of wine, which is an important element of the Mediterranean diet as such, has positive consequences on the general health of the one who consumes it – surely within the context of a balanced diets and regular physical activity-. Communication campaigns aimed at educating the public to the benefits of moderate consumption of every product should be considered, given the fact that promoting the absolute abstention of any product never resulted in the expected outcome.

Recommendations

In this complex context, us, European wine farmers, have been acting in our best efforts, trying to come up with creative ideas by strengthening our adaptability. However, we have been feeling the absence of our long-standing partner in the success story that European wine has become. The European Commission in these past months has remained silent and deaf to our calls. Whatever the threat, being the Covid pandemic, climatic disasters, trade war, Brexit, the only answer that we have been receiving from its services is “there is simply no money”, answer that has been reiterated recently after the frost wave.

This answer is simply not credible nor understandable, considering the amounts of funds that the EU has moved for other strategic sectors and the importance of the economy generated by our industry for more than 50 regions and the EU in general, representing 2.5 million works, more than half of the European trade balance, and the image of the EU agri-for products, whose wines are the best ambassadors.

A renewed private-public partnership as secret of success

The duo private-public has shown its potential when cooperating over the last two decades, putting back on promising track the wine economy, overcoming the challenge of the new world production. It is now the time to write a new success story, building the foundation of a new cooperation for the benefit of jobs, economy, environmental features and protection, and European identity.

It is therefore urgent for the European Commission to take actions, complementary to those initiative taken at local, regional, or at national level.

Farm Europe welcomes the agreement on the reform of the Common Agricultural Policy reached today. It preserves the common dimension of this policy and it provides the means to give impetus to a real economic and environmental ambition, clearly improving the European Commission’s initial proposal.

The tireless work of the Portuguese Presidency, of long-established MEPs such as Peter Jahr, Anne Sander, Paolo de Castro, Nobert Lins and Herbert Dorfmann, and of newcomers in the European Parliament CAP negotiations such as Martin Hlavácek,Pascal Canfin, Pina Picierno, Jeremie Decerle and Irène Tolleret, each of whom played a key role in structuring constructive and ambitious positions within the European Parliament and then in the inter-institutional negotiations must be commended.

The final compromise provides a clear framework for Member States to implement a strategy for the economic and environmental transition of the agricultural sector in order to provide quality food for all Europeans and to allow farmers to invest and innovate, using the following tools:

With the “eco-schemes“, the European Union now has an its disposal an incentive tool to help European farms to adapt to climate change, store carbon, enrich biodiversity, be less dependent on inputs and enhance animal welfare. This tool will prove its effectiveness when used to achieve the twin goals of more economically and environmentally efficient farming. The point-system should ensure a level playing field across Europe and within Member States in the ambition and implementation of the different eco-schemes.

With “green investments” earmarked as a priority in the second pillar of the CAP, and the ability of all sectors to implement operational programs funded by the first pillar of the CAP, this reform sends the signal that it is through innovation and investment that the European Union will succeed in achieving the ambition set in the Farm to fork Strategy and the Green Deal. These investments must make it possible to achieve the environmental objectives while gaining in economic competitiveness and preventing competition from third countries to develop.

With the crisis reserve of at least €450 million and the possible earmarking of 3% of the first pillar of the CAP for risk and crisis management tools, the economic nature and reactivity of the CAP in response to unforeseen events are potentially reinforced. It will be important for the Member States to seize these levers and for the Commission to activate the tools at its disposal in the event of a crisis without delay and without procrastination.

On this basis, the European agricultural sector has a certain visibility, which is imperative for the years to come, with a strong responsibility now resting on:

the shoulders of the Commission to validate the national strategic programs by ensuring their consistency with the guidelines defined at European level and by limiting the distortions that could arise from divergent approaches between Member States.

the shoulders of the Member States to fully activate the tools designed by the European Parliament and the Council in order to strengthen the European agricultural sectors and prepare their future by putting a clear priority on innovation investments and risk management.

the shoulders of the co-legislators to make sure that the regulations of the F2F reinforce the orientations decided by the co-legislators in the CAP and do not contradict them.

It is regrettable, however, that food chain issues, notably those related not only to digitalization and blockchain, but also to the food and nutritional dimension in particular, have not found their place in this reform. It is to be hoped that these topics will be addressed in an effective and coherent way with the CAP in the framework of future proposals from Farm to Fork, in order to meet the expectations of all consumers, by rejecting the model of a multi-speed food supply according to purchasing power.

The month of May 2021 was marked by repeated calls for aid measures from countries affected by the frosts in March and April. In particular Italy, France and Greece asked the European Commission for appropriate aid. Moreover, the Council of Ministers outlined a proposal (as part of the CAP reform) envisaging the authorisation of the total or partial elimination of alcohol in the context of oenological practices, sparking a discussion at EU- level.

On a national level, in Italy CMO, planting rights and non-alcoholic wines were discussed in a hearing in the Senate; exports in the UK plummet in the first months of the year, while Italy observes an increase in large-scale retail trade in the same period.

News have circulated that the UK-Australia Free Trade Agreement (FTA) is reaching the final legs of negotiation.

The UK would have offered full free access to its market, including in beef and sheep, with a phasing-out of quotas and tariffs for these two sectors in 15 years. It is also rumoured that the UK would accept to reduce the phasing-out to only 10 years.

Our British friends will excuse us, but this note will focus on the knock-on effects into the EU agriculture, and in particular the beef sector.

A 10 years phasing-out on all import restrictions will likely consist of initial quotas being gradually increased, till full liberalization. The impact will depend on the size of the quotas (and less significantly on the in-quota tariff rates); and on whether or not the out-of-quota tariffs will also be gradually reduced.

It should be noted that at a certain point in time it will become profitable for the Australians to export their beef out-of-the –quota to the UK, paying whatever will be the full tariff, as the volumes exported under the quota make the overall exports economically viable.

Thus, in a shorter period of time than the 10 years foreseen, the quantities of Australian beef sold in the UK market will be similar to those under full free trade.

What happens to our exports of beef to the UK? They will face dramatic competition from cheaper Australian cuts, and their UK market will shrink accordingly.

This is no minor effect, as the UK is the top destination for Irish beef exports, over 1 billion euros annually. Ireland will be faced with the losses in the UK market and the difficulties in finding other export markets outside the EU that could compensate for those losses.

Inevitably a good part of prior UK exports will land in continental Europe, competing with other EU producers in a stagnant market, under pressure from all sides ( F2F, methane emissions, recommended diets).

Farm Europe has warned since Brexit was voted by the UK that, even with a fully-fledged EU-UK FTA, the EU agri-food sector would lose market share in the UK as a result of the UK opening up its market to other countries. So this does not come as a surprise, but the negative impact is coming closer with a CAP reform process coming to an end without fully integrating this new major challenge for the years ahead.

As bad news rarely fly alone, the fact that the UK is willing to phase-out all import restrictions on beef to Australia will set the tone for the remaining UK FTAs under negotiation. Specifically, it will flow logically that the US will accept no less. Therefore what we are saying about the impact of Australian imports will be compounded by US exports in the future.

This note focus on the beef sector. But we also know that the UK is willing to enter the Trans-Pacific Partnership Free Trade Agreement (TPP). Other sectors, like dairy, poultry and sugar, would benefit from preferential access conditions to the UK market. Top world exporters are part of the TPP – New Zealand for dairy, just to give an example. And again, this would have a negative knock-on effect on our exports to the UK.

There is very little we in the EU can do about decisions that are made in the UK. The best way to absorb the shock is to become more competitive, to conquer more export markets, in other words to be very strong and resilient economically. However, what we are witnessing as proposals coming out of the European Commission has the opposite effect, piling up further restrictions and increasing producing costs. It is urgent to change course, and address environmental and other issues using science, and mobilizing technologies and resources to achieve our objectives without making us all poorer and ultimately more dependant on imports.

For those who are not familiar with the Taxonomy Regulation, it aims at “launching an ambitious and comprehensive strategy for sustainable finance with the aim of redirecting capital flows to help generate sustainable and inclusive growth”.

A draft Delegated Act “establishing the technical screening criteria for determining the conditions under which an economic activity qualifies as contributing substantially to climate change mitigation or climate change adaptation and for determining whether that economic activity causes no significant harm to any of the other environmental objectives” was now leaked, shedding light on the intentions of the Commission services.

On biogas and biofuels the draft Delegated Act sets out the relevant criteria. They should normally be in line with the existing criteria for sustainability spelled out in the Renewable Energy Directive (RED II).

But although there is a dutiful link to the RED II, the following sentence is added up in the Annex I –point 4.13: “Food-and feed crops are not used for the manufacture of biofuels for use in transport.”

On which grounds do the Commission services go beyond what is actual EU law on the sustainability of biofuels? On which grounds do they depart from the sustainability criteria spelled out in RED II?

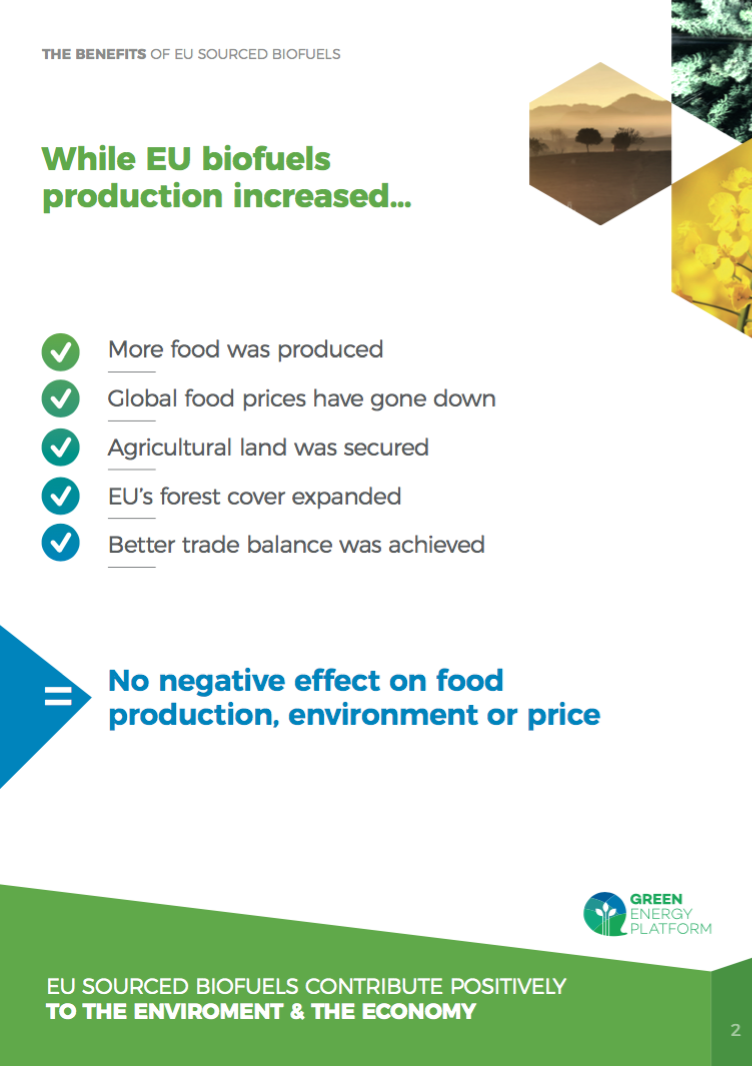

What are the facts that underpin excluding sustainable crops? The Commission herself has recently acknowledged that EU crop based biofuels are sustainable. No impact on food and feed prices, no environmental downside.

On the contrary, those biofuels that would now be excluded are by far and large the main contributor to decarbonizing the transport sector. On top of promoting employment in rural areas, sustaining farmers’ incomes and improving the availability of high quality protein for animal feed.

How do the Commission services want to reach the new ambitious targets of decarbonisation of the transport sector, within the EU Green Deal, if they wish to cut those sustainable biofuels from the benefits of sustainable finance?

The sentence is thus tantamount to “shooting ones feet”. It shatters the potential of sustainable biofuels to decarbonize transport. It should be erased.

This paper aims to cast a light on the nexus between the profitability of rural livelihoods and biofuels within the EU. In doing so, it focuses on putting the deep and structural relationship between rural labour and biofuels into a data driven perspective to highlight what is rarely discussed: the low wages within the farming sector and the reality that without biofuels, this situation would be even worse.

Summary

There is no plausible coherence in the positions of policymakers who simultaneously extoll higher minimum wages, argue that the EU should grow more food and malign biofuels—even though some would like to present it as a consensus position in Brussels. The only way to reconcile these positions in the European Green Deal is to re-evaluate biofuels based on actual 2020 data and then promote a gradual increase in biofuels.

The role of biofuels in markets has been treated by researchers simplistically, much as minimum wage was for most of the last century. These simplistic approaches are not only wrong, but they are wrong for exactly the same reasons that the minimum wage arguments were wrong.

Enough data now exists for a more mature approach to the role biofuels play in the economy.

EU farmers earn on average €20k annually. Three quarters of all farms are family enterprises that have an even lower average income. This explains as well why farms have been abandoned at high rates in the last decade.

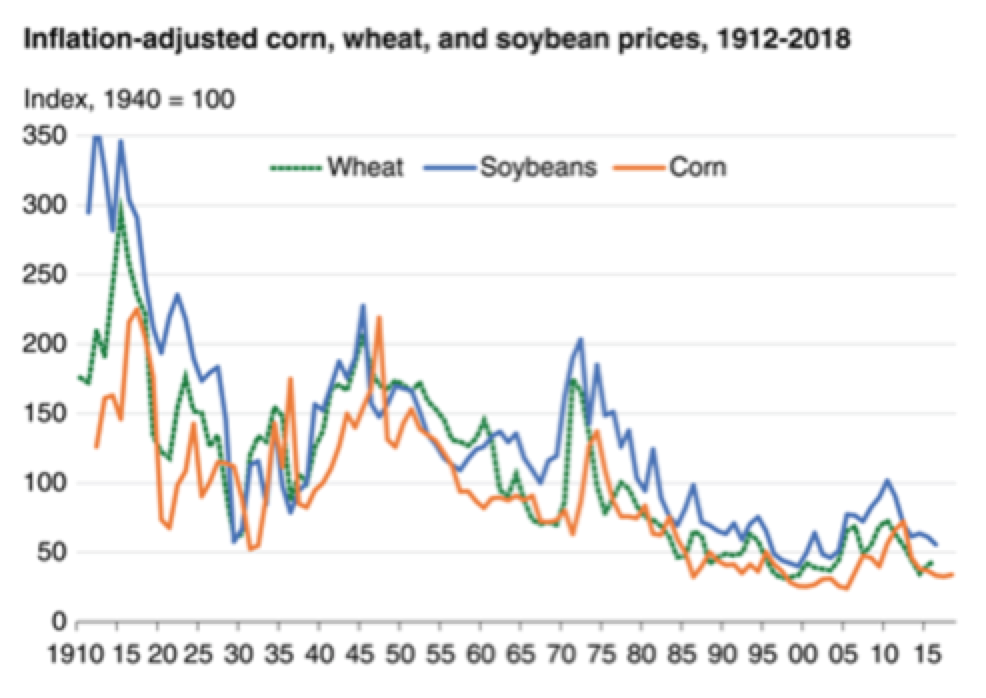

The main reason for low farm incomes is the low market price of agricultural products. Real prices of corn, wheat, rapeseed, barley, rye, triticale, sugar beets, sunflower and soy have been declining since the 1950s. Productivity growth has not kept up with the decline in real prices.

Since the average age of farmers in the European Union is between 50 and 60 and increasing, the rate of farm abandonment may dramatically increase through 2030.

The way to improve farm incomes is to increase demand for farm products.

Biofuels have in the past provided price support for basic agricultural products in the EU, without causing any harm to food market. Although not enough to reverse the trend of price erosion.

As recognized by the Commission itself, earlier predictions of Commission policy makers for EU sourced biofuels in 2020, pointing to higher food prices or adverse land and environmental impacts, were incorrect.

The Commission recognises as well the importance of EU biofuels to the economy, and to reducing GHG emissions

An increase in biofuels use in the European Union to 2030 is the obvious choice to advance social, climate and economic priorities.

The paper first explains the recent evolution of farm profitability in the EU and point out that the EU has struggled to give meaningful answers to live up to its obligation on safeguarding a reasonable living for the European Union farmers. One significant contribution in this aspect is the role that EU biofuels play and could offer, hence the paper then proposes a policy direction to follow.

Evolution of farm profitability in the EU

European farmers struggle to eke out a living. One of the goals of the Common Agricultural Policy (CAP) is to safeguard European Union farmers to make a reasonable living. Studies show that profitability in agriculture was and currently still is a major problem.

While there are indeed huge differences between the farm income of Member States or the various types of farming, some trends can be observed:

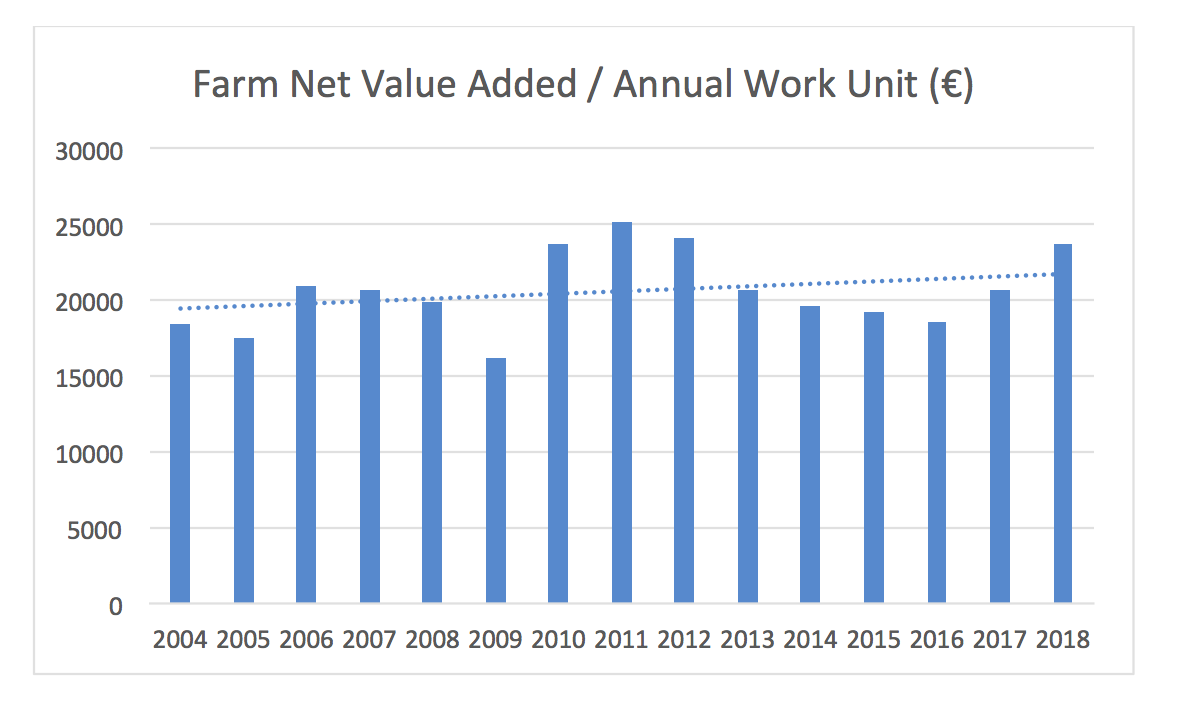

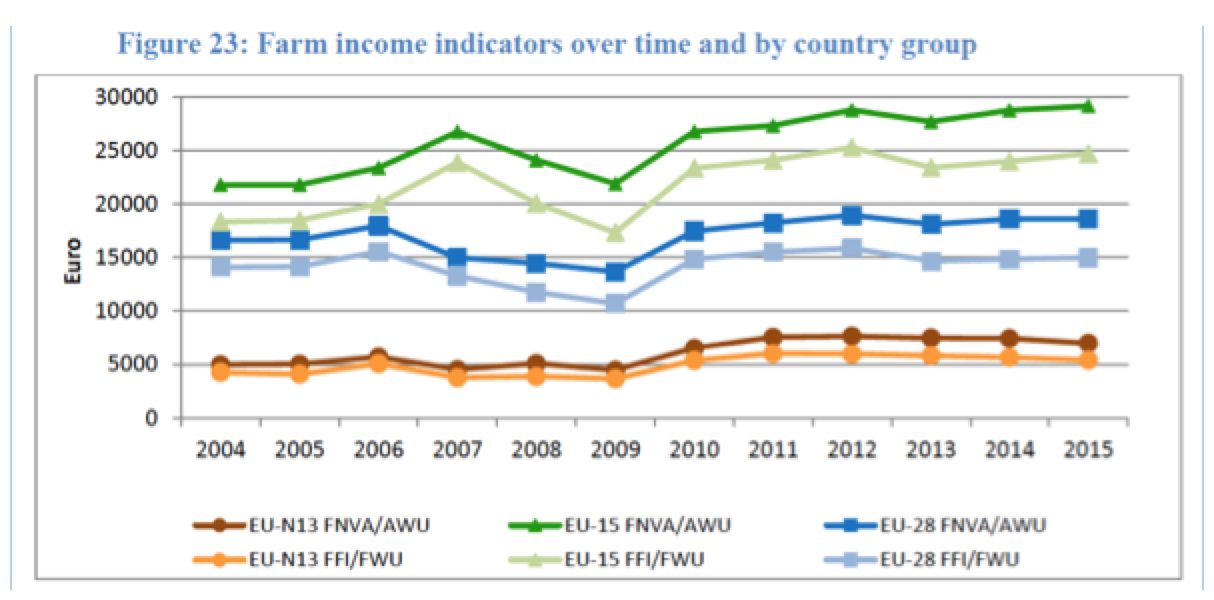

Farm Accountancy Data Network (FADN) provides sample farm data that is probably the best available on farm profits. A 2018 EU report based on FADN, “EU farm economics overview”, focuses on Farm Net Value Added (FNVA) as an indicator of profitability. FNVA is usually expressed per Annual Work Unit (AWU), which can be seen as a measure of labour productivity.

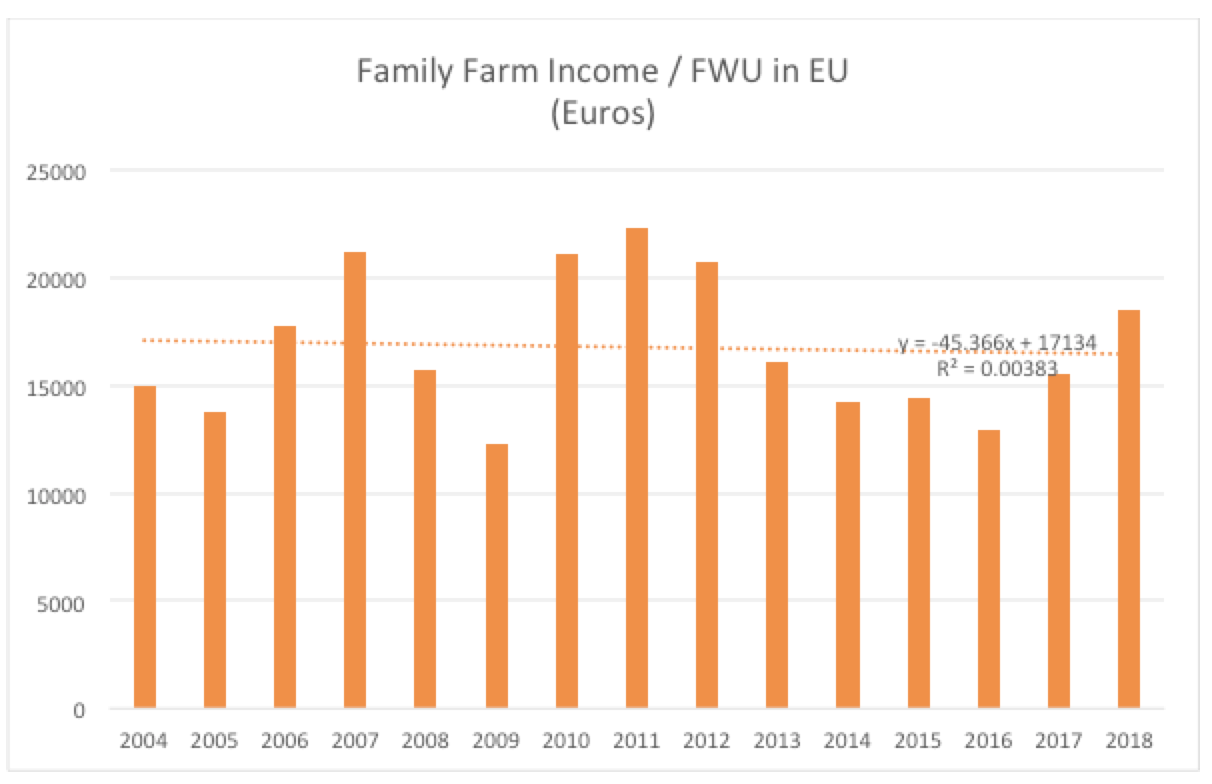

The chart below shows the evolution of FNVA, i.e. gross farm income minus depreciation costs. It is presented by labour unit, so differences in farm sizes are taken into account. Only field crops are included in the chart, albeit not much of a difference across farm types. It shows that the annual income per farmer in the EU has been about €20k.

An alternative measure of agricultural income is Family Farm Income (FFI), as a high proportion of work in the agricultural sector (about 75%) is carried out by family members. FFI is expressed per family work unit (FWU), and is calculated by deducting from FNVA the costs of wages, rent, interest, and the opportunity costs of own capital, so that we arrive at the remuneration of family labour. At the EU-28 level, the average farm family income expressed per family labour unit (FFI per FWU) stood at €18.5k in 2018. Notably, between 2004 and 2018 FFI per FWU did not increase.

In comparison, the net annual earnings of an average working couple with two children were EUR 50 500 in the EU-27 in 2019.

Since an income of €15-20k is not an appealing prospect, it is no surprise that young farmers are few in number. Moreover, farm income is around 40% lower than non-agricultural income. Lastly, the farm income has been mostly flat in the past decade despite a decrease in the number of farmers and an increase in average farm size.

Source: DG AGRI, Farm Accountancy Data Network (FADN)

The aging of farmers is a serious problem. The average age of farmers was 49.2 in 2004, but 51.4 years in 2014. In 2016, almost one third (32.8 %) of all farm managers in the EU-27 were 65 or over. Only 11% of farm managers in the EU were under 40.

Without even mentioning the drastic effects of what climate change will bring or the economic downturn and business uncertainties caused by the Covid-19 pandemic, these indicators only lead towards one conclusion: a bleak picture regarding the future of the next farming generation and that thus farm abandonment may dramatically increase through 2030. In order to change this negative trend and overcome these challenges, farmers need reinforced tools to be able to be profitable once again.

A European Parliament study finds that ‘structural statistics for EU agriculture make it clear that many farmers (at least a third, and more if other members of their household are included) also have other gainful activities. National results where available show that other incomes not only raise the household income levels of farm families, but also add to its stability.’ In other words, many farmers rely on other incomes as revenue from farming alone is insufficient to maintain a decent standard of living.

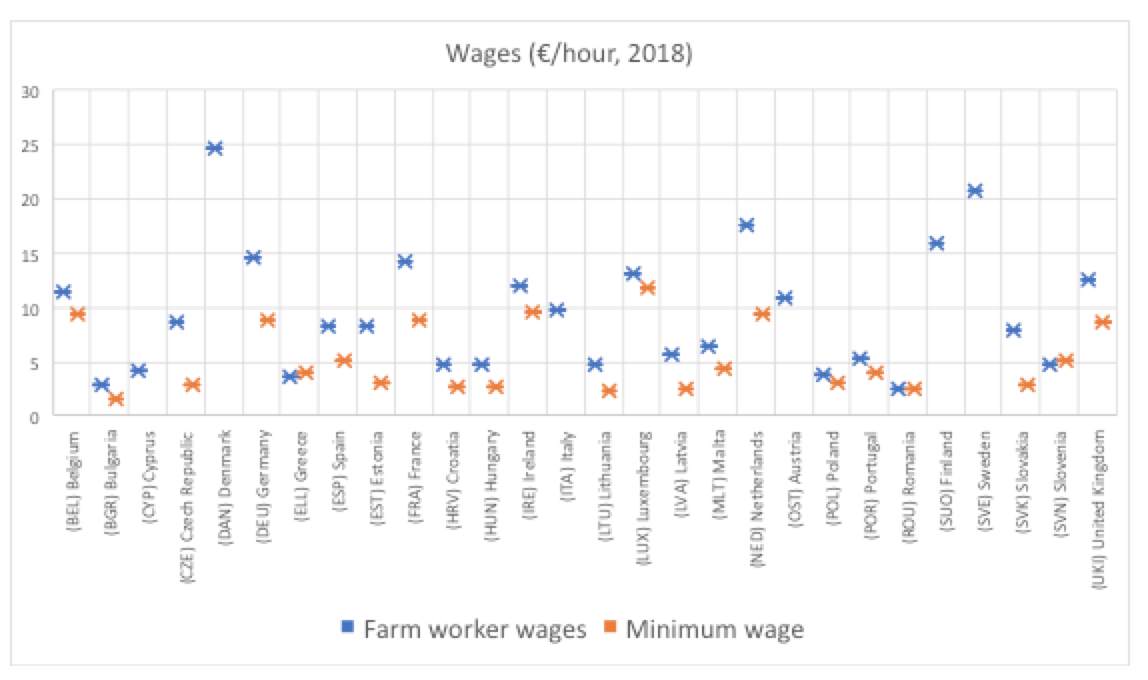

The EU Farm Economics Overview (2018) found that the average hourly wage of farm workers was €7.90 in the EU-28 in 2015. Eurostat reported €23.1 as the EU’s average hourly wage in 2017. Farm worker wages are close to the minimum wages in most EU countries (see chart below). In Greece and Slovenia, farm workers earned less than minimum wage in 2018.

In short, farmers and their employees struggle to earn a decent living, and farming presents economically bleak prospects to a younger generation that has other options. This has all resulted in the fact that from 2008-2018 2.3 million farmers left the sector and were not replaced. Some of their land remained in agriculture through farm consolidation but a significant amount was just simply abandoned.

One must not forget the combined effect of stiffer price competition, rising costs and volatility plus public aids whose real value decreases each year.

Finally, taking into account the European Commission’s initial Common Agriculture Policy reform proposals it forecasted that farmers’ incomes are bound to drop by a staggering 14% (in real terms) in the next decade when the Farm to Fork Strategy is already considered to rearrange the status quo.

All this proves that farm profitability needs to be at the heart of agricultural policies if the true objective is to conjugate the revival of European rural regions. In that respect, coordination of policies focusing on farming, climate and energy policies is necessary.

Inflation-adjusted prices for corn, wheat, and soybeans and other basic agricultural commodities show long-term declines. Increased productivity in crop production underlies a general decrease in inflation-adjusted prices over the past century (see chart below).

In conclusion the only way to improve farm incomes, other than subsidies, is to increase demand for the products that farms produce. Unless being able to hope for a reasonable living more and more farmers will decide to leave the sector. This would have a devastating impact on the countryside, as farmers won’t be there to deliver any more of their caretaking or public good services, which are not normally paid for by the markets.

The role of biofuels

On the other hand, crop-based biofuels offer a way to provide price support to farmers with declining incomes. Unsurprisingly therefore farmers and farming associations support biofuels in Europe.

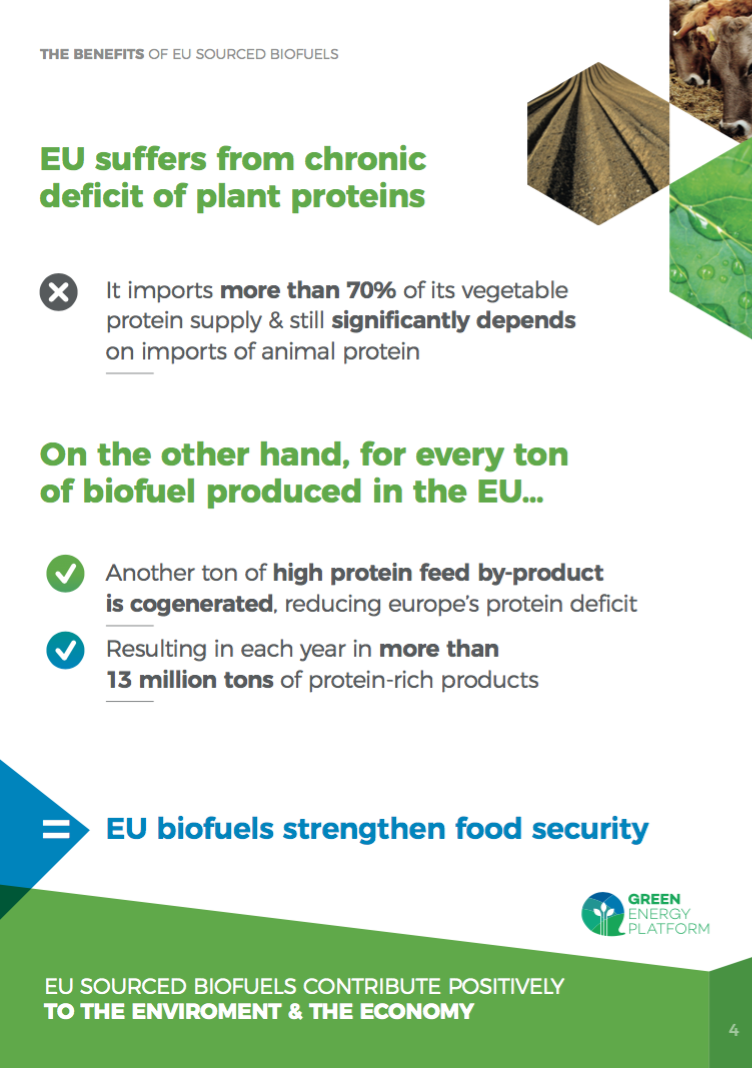

Farmers find that conventional biofuels make it easier to manage agricultural commodity markets, which can help stabilise agricultural commodity markets and prices, as well as providing greater security for consumers and farmers. Farm Europe notes that biofuels produced from EU feedstock (mostly from colza, maize, sugar beet and wheat) generate at least 6.6 billion euros of direct revenue for EU farmers.

Even at their moderate volumes in the EU today biofuels have not actually increased agricultural prices. The 2017 EU Renewable Energy Progress Report finds that “EU ethanol consumption had negligible impact on cereal prices”. The report also notes that lower biofuel demand for vegetable oils was a factor contributing to the fall in oils/fats prices.

Arguably, without biofuels, demand for farm products would be even lower, further aggravating the situation.

As an Irish farmer representative put it “without the ability to make income farming goes nowhere and the next generation won’t be there”, stressing the pressure on incomes and the lack of markets to consume their products. In short, markets need to be preserved and created for farmers outside the Common Agricultural Policy’s subsidies.

As Copa-Cogeca, CEPM, FEDIOL and other farming associations stated producing biofuels from arable crops in the EU has opened up new agricultural commodity markets for European farmers. Biofuel production has encouraged investments on farm and into agricultural research, which in turn has allowed yields to be increased through improved techniques and new crop varieties. This is found to be beneficial for the production of food, feed and biofuels.

Further, European produced biofuels reduce by 13 MT dependency on imports of proteins used in animal farming (soy from the Americas), by supplying animal feed as co-product.

Moreover, jobs are created and maintained mostly in rural neighbourhoods – IRENA finds that 239 thousand jobs were supported directly and indirectly in the European Union by the production of liquid biofuels in 2018-2019.

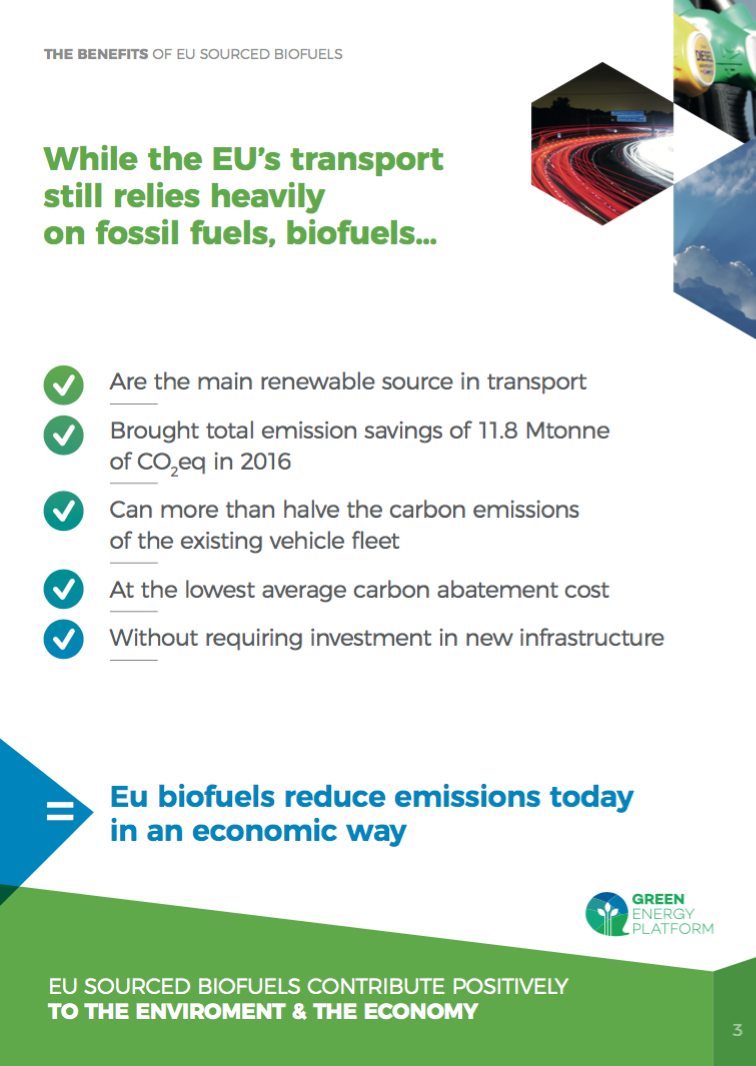

Last but not least, biofuels have contributed more to effect transport decarbonisation than anything else over the past decade.

Policy direction to follow

Policy issues are not black and white.

A mix of over-simplified economic theory and improperly applied ideology has misled a plurality of EU policymakers to believe that crop based biofuels present no benefits, even though evidence in 2020 makes that position entirely indefensible. Moreover, the evidence in 2020 makes clear that whatever the right balance is for crop-biofuels use in the EU, current volumes are too little.

Extreme arguments have been mobilised, such as suggesting replacing all transport fuels with biofuels. However, business and industry, along with most policymakers, do not support these extremities. Moderation and context are sorely needed in the biofuels debate. This implies a profound change of mind of some influencers and decision makers and a change as well in the types of public actions. It is about leaving a world of dogmas and assumptions that have been flourishing for more than a decade in order to redefine an ambition based on science, pragmatism and the will to move forward together without stigmatizing each other but accompanying the progress and the necessary transitions.

An increase in biofuels use in the European Union to 2030 is the obvious choice to advance social, climate and economic priorities.

Without biofuels, farming in Europe is likely to continue to decline—resulting in job losses and the EU will miss its objectives of decarbonisation of transport notably.

As is the case for its agriculture as a whole, the EU shall not limit itself to a series of initiatives aimed at accompanying a slowdown for biofuels but it must focus on launching dynamic economic strategies within agriculture to boost investment across the EU.

The decade between 2020 and 2030 should be used to tap the potential in biofuels to strengthen farming, by providing a stable market outlet – making the prospect of farming more alluring to young farmers and thus enhancing the role of agriculture becoming a provider of a decarbonized economy.

The EU agri-food promotion policy is a very important tool to expand sales and increase penetration in international markets.

In the current times, marked by the negative effects of the Covid-19 crisis in some key sectors and uncertainty on the future outlook, farmers are even more eagerly reliant upon the boost that promotion programmes bring to agri-food sales.

It came thus as a surprise that the Commission intends to reserve a lion’s share of the available funds to only promote organic products. The Commission indicated to the European Parliament AGRI Committee that 50% of the funds would be reserved to contributing to the objectives of the Farm-to-Fork strategy, organic products first and foremost.

Farm Europe sees two fundamental problems in this approach.

First, as organic production represents close to 10% of the whole value of agriculture production, what is the justification to treble its share in the promotion programme to the detriment of the majority of farmers? EU agri-food products are healthy and recognized as top quality worldwide, why discriminate against most producers in the allocation of promotion funds? Not to mention that the promotion of organic products in the EU will also boost imports of products labeled as organic, from a host of third countries.

Second, we see a serious institutional problem as the Commission imposes its proposals (Green Deal, Farm-to-Fork) before they are endorsed by the co-legislators – the European Parliament and the Council. The basic promotion Regulation was adopted by the co-legislators, as it was the allocation of CAP funds. On which grounds does the Commission skew the programme to adhere to its non-adopted proposals? Unfortunately, this seems to become a pattern, as the Commission has also indicated that it intends to impose its Green Deal, Farm-to-Fork and Biodiversity Strategies in the CAP Strategic Plans, before they are EU law.

The Commission also points out to renewed scrutiny of the promotion of alcoholic beverages and red meat. On which scientific basis? Important segments of the wine and meat sectors have been particularly affected by the Covid-19 crisis, they should thus come high in the 2021 promotion programme, not the opposite.

The Commission 2021 Promotion Policy flaws should be reversed and adhere to its basic objectives, without discriminating against most producers and overstepping institutional powers.

The Green Energy Platform, launched in the summer of 2017, brings together the players in the agricultural sector that see European agriculture not only as a source for food and feedstocks but also as a green energy supplier. We would like to draw the attention on the contribution and importance of this critical European infrastructure and sector in these crucial times and for the future as well.

The Communication from the Commission on the European Green Deal states that“to deliver the European Green Deal, there is a need to rethink policies for clean energy supply across the economy” including for transport and food & agriculture, yet the latest Commission data tells us that we are still far behind from the desired objectives.

The transport sector poses one of the greatest challenges to the Green Deal. Moving forward will require an advanced mobilization of additional input of renewable energy sources.

A key instrument shall be the further contribution of EU sourced biofuels, which are sustainable and help to achieve the EU’s climate targets by decarbonizing the transport sector, as the latest Commission data certifies accordingly.

In order to tackle the immense challenges ahead, the EU needs to realize that European biofuels make an essential contribution to Green Deal, and therefore bring back EU sourced biofuels into the Green Deal discussion, as they are an effective response for concrete and rapid benefits towards the environmental and transformative ambitions of the Green Deal.

The following leaflet summaries some of the key facts for EU sourced biofuels such as:

not having a negative effect on food production, environment or price

The Commission has just published a Communication on the EU Trade Policy Review.

The fundamental approach to trade issues is kept unchanged. The key word is openness: “The EU is built on openness, both internally and externally. It is the biggest exporter and importer of goods and services worldwide.”

The Covid crisis talk on relocalisation of key industries, strengthening the resilience of the EU’s economy, is by far and large forgotten. According to the Commission: “Trade policy can contribute to resilience by providing a stable, rules-based trading framework, opening up new markets to diversify sources of supply, and developing cooperative frameworks for fair and equitable access to critical supplies.”

Thus it comes as no surprise that the Commission basically advocates continuity.

The new elements of greater relevance are linked to the Green Deal adequacy of the trade policy: ” The EU will propose that the respect of the Paris Agreement be considered an essential element in future trade and investment agreements. In addition, the conclusion of trade and investment agreements with G20 countries should be based on a common ambition to achieve climate neutrality as soon as possible and in line with the recommendations of the Intergovernmental Panel on Climate Change (IPCC).”

In addition it advocates “autonomous measures… supporting the objective to ensure that trade is sustainable, responsible and coherent with our overall objectives and values. The Carbon Border Adjustment Mechanism (CBAM) is a case-in-point.”

Knowing that a CBAM needs cooperation and agreement of other WTO members, in order not to expose the EU to retaliatory measures, we seem to be still a long way from that happening.

Having said that, the reference to restricting climate neutrality conditions to trade and investment agreements to G20 countries only, seems to indicate that the EU will not ask most countries to mirror its efforts on climate change. Whilst G20 economies account for a large share of the world economy, it shouldn’t be forgotten that big exporters of agriculture products are outside the G20, as Thailand, Chile, Uruguay, New Zealand, or Ukraine.

As the Commission is proposing a host of internal climate and environmental measures – F2F and Biodiversity Strategy are good examples – it seems to accept that many other countries will not have to enforce similar goals or face additional import duties. How can the EU then avoid carbon leakage through increased imports, including of agriculture products? How can EU farmers and the agri-food sector fairly compete, when facing more restrictions and additional burdens that many of their competitors?

By the same token, the Communication is vague on what the Commission understands as seeking a level playing field in trade. Producers in countries with substantially lower environmental standards will put EU producers into a clear disadvantage, but the Communication fails to recognise the problem.

What is also striking is what is not in the Communication. The EU food security is not mentioned, and that leaves little doubt that the Commission believes the best model to contribute to the resilience of the economy is open and freer trade under multilateral rules, without considering its potential negative impacts when appropriate.

The fight against imported deforestation is not mentioned either. Although the EP has asked the Commission to act, there are only vague indirect references to corporate diligence and Mercosur commitments.

The negative effects of competitive devaluation is also absent, although its impact is often larger than import tariffs, enabling third-country exporters to undercut EU market prices.

Farm Europe argues that the time has come to adopt a more balanced trade policy. After Covid-19 we need a change of policy that does not compromise food security. We need a better balance between the benefits of freer trade and its asymmetric negative impacts. We need less of an ideologically driven policy and more pragmatism and realism.